Status of the Social Security and Medicare Programs

A SUMMARY OF THE 2023 ANNUAL REPORTS

Social Security and Medicare Boards of TrusteesThe Trustees of the Social Security and Medicare trust funds report on the current and projected financial status of the two programs each year. This document summarizes the findings of the 2023 reports. As in prior years, we found that the Social Security and Medicare programs both continue to face significant financing issues.

Based on our best estimates, this year's reports show that:

• The Hospital Insurance (HI) Trust Fund will be able to pay 100 percent of total scheduled benefits until 2031, three years later than reported last year. At that point, the fund's reserves will become depleted and continuing program income will be sufficient to pay 89 percent of total scheduled benefits.

• The Old-Age and Survivors Insurance (OASI) Trust Fund will be able to pay 100 percent of total scheduled benefits until 2033, one year earlier than reported last year. At that time, the fund's reserves will become depleted and continuing program income will be sufficient to pay 77 percent of scheduled benefits.

• The Disability Insurance (DI) Trust Fund is projected to be able to pay 100 percent of total scheduled benefits through at least 2097, the last year of this report's projection period. By comparison, last year's report projected that the DI Trust Fund would be able to pay scheduled benefits through at least 2096, the last year of that report's projection period.

• If the OASI Trust Fund and the DI Trust Fund projections are added together, the resulting projected fund (designated OASDI) would be able to pay 100 percent of total scheduled benefits until 2034, one year earlier than reported last year. At that time, the projected fund's reserves will become depleted and continuing total fund income will be sufficient to pay 80 percent of scheduled benefits. (The two funds could not actually be combined unless there were a change in the law, but the combined projection of the two funds is frequently used to indicate the overall status of the Social Security program.)

• The Supplemental Medical Insurance (SMI) Trust Fund is adequately financed into the indefinite future because, unlike the other trust funds, its main financing sources--premiums on enrolled beneficiaries and federal contributions from the Treasury--are automatically adjusted each year to cover costs for the upcoming year. Although the financing is assured, the rapidly rising SMI costs have been steadily increasing demands on beneficiaries and general taxpayers.

Since last year's reports, projected long-term finances of the OASI and the OASDI Trust Funds worsened due to the Trustees revising down the expected levels of gross domestic product (GDP) and labor productivity by about 3 percent over the projection window. The Trustees made this change as they reassessed their expectations for the economy in light of recent developments, including updated data on inflation and U.S. economic output.

Despite the downward revision to economic assumptions, the projected long-term finances of the HI Trust Fund improved since last year’s report. The improvement is mainly due to lower projected health-care spending stemming from updated analysis that uses more recent data.

SMI Trust Fund expenditures for Medicare Part B as a share of GDP are also projected to be lower than previously estimated in part for the same reason. In addition, expenditures on drugs under SMI in Medicare Parts B and D are projected to be markedly lower as a share of GDP due to the impact of provisions of the Inflation Reduction Act, which became law in August 2022.

Lawmakers have many options for changes that would reduce or eliminate the long-term financing shortfalls. We urge Congress to consider such options for both Medicare and Social Security, like the proposal for Medicare in the President’s FY24 Budget. With each year that lawmakers do not act, the public has less time to prepare for the changes.

By the Trustees:

Secretary of the Treasury,

and Managing Trustee of the Trust Funds.

Xavier Becerra,

Secretary of Health and Human Services,

and Trustee.

Acting Secretary of Labor,

and Trustee.

Kilolo Kijakazi,

Acting Commissioner of Social Security,

and Trustee.

INTRODUCTION

This summary of the 2023 Trustees Reports describes the outlook for both the Social Security and Medicare programs and the projected actuarial status of the trust funds that finance them. It presents results based on the Trustees’ best estimates of likely future demographic, economic, and program-specific conditions, which are referred to as the intermediate set of assumptions in the Trustees Reports.1

Trust fund depletion dates are a common way of tracking the status of the trust funds since, if annual income is not sufficient, full scheduled benefits in the law cannot be paid after trust fund asset reserves are depleted. Asset reserves are projected to become depleted in 2033 for OASI, a year earlier than in last year’s report, and in 2031 for HI, three years later than in last year’s report. Starting at those dates, less than full scheduled benefits would be payable. The DI Trust Fund is projected to be able to pay full benefits through the end of the long-range projection period (2097 in this year’s report).

Another measure of the status of the trust funds is called the “actuarial balance.” 2 A negative actuarial balance is called an actuarial deficit and represents a shortfall in financing; a positive actuarial balance is called an actuarial surplus. OASI and HI have actuarial deficits over the next 75-year period while the DI Trust Fund has a small actuarial surplus.

Table 1 lists the 2023 Trustees Reports’ key findings for each of the separate trust funds established under the law.

| Social Security | Medicare | |||

|---|---|---|---|---|

| OASI | DI | HI | SMI | |

| Type of benefit paid from the trust fund | Retirement and survivor benefits | Disability benefits | In-patient hospital and post-acute care (Part A) | Physician and out-patient care (Part B); prescription drugs (Part D) |

| Full scheduled benefits are expected to be payable until | 2033 | At least through 2097 | 2031 | Indefinitely |

| Percentage of scheduled benefits payable at time of reserve depletion | a77 | — | b89 | — |

| 75-year actuarial balance, as a percent of taxable payroll | -3.62 | 0.01 | -0.62 | — |

a The percent of scheduled benefits payable is projected to decline to 71 percent by 2097.

b The percent of scheduled benefits payable is projected to decline to 81 percent by 2047 before gradually increasing to 96 percent by 2097.

It is often useful to consider the findings for the two Social Security trust funds (OASI and DI) on a combined basis. The actuarial deficit for Social Security as a whole – called OASDI – is 3.61 percent of taxable payroll. If these two legally separate trust funds were combined, then the hypothetical OASDI asset reserves would be projected to become depleted in 2034 and 80 percent of scheduled Social Security benefits would be payable at that time, declining to 74 percent by 2097.

BACKGROUND

What are the Trust Funds? There are four trust funds that hold Social Security and Medicare program income. The asset reserves held in the trust funds and program income from dedicated financing sources, such as the payroll tax, are used to pay the programs’ benefits. Each trust fund pays only the types of benefits it is permitted to pay under law. These trust funds were established by Congress and are managed by the Secretary of the Treasury.

The four trust funds are:

• Old-Age and Survivors Insurance (OASI) Trust Fund

• Disability Insurance (DI) Trust Fund

• Hospital Insurance (HI) Trust Fund

• Supplementary Medical Insurance (SMI) Trust Fund

The OASI and DI Trust Funds are distinct legal entities and operate independently. The two funds are sometimes considered on a combined basis, referred to as OASDI, to illustrate the status of the Social Security program as a whole.

The only disbursements permitted from the funds are benefit payments and administrative expenses. The Trustees must invest all excess funds in interest-bearing securities backed by the full faith and credit of the United States. The Department of the Treasury currently invests all program revenue in special non-marketable U.S. Government securities, which earn interest equal to rates on marketable securities with durations defined in law.

The balances in the trust funds represent the accumulated value, including interest, of all prior program annual surpluses and deficits.

How are the Social Security and Medicare programs financed? Under current law, the ways the programs are financed differ by type of benefit.

OASI and DI Financing

OASI and DI are financed almost exclusively by payroll taxes, income tax on Social Security benefits, and interest on trust fund asset reserves.

OASI and DI receive most of their income from payroll taxes. Payroll tax contributions consist of taxes paid by employees, employers, and self-employed workers. Self-employed workers pay the equivalent of the combined employer and employee tax rates.

| OASI | DI | Total OASDI | |

|---|---|---|---|

| Employees | 5.30 | 0.90 | 6.20 |

| Employers | 5.30 | 0.90 | 6.20 | Self-employed workers | 10.60 | 1.80 | 12.40 |

Current law establishes payroll taxes for OASI and DI, which apply to earnings up to an annual maximum ($160,200 in 2023). The maximum usually increases each year as the national average wage increases.

Who Pays Income Tax on Their Social Security Benefits?

Social Security beneficiaries with incomes above $25,000 for individuals (or $32,000 for married couples filing jointly) pay income taxes on up to 50 percent of their benefits, with the revenues going to the OASI and DI Trust Funds. Those with incomes above $34,000 (or $44,000 for married couples filing jointly) pay income taxes on up to 85 percent of benefits, with the additional revenues from taxation of more than the first 50 percent going to the HI Trust Fund.

HI Financing

Medicare HI receives financing from payroll taxes, income tax on Social Security benefits, premiums, and interest on trust fund asset reserves.

HI receives most of its income from payroll taxes. Federal law establishes the payroll tax rates for HI.

| HI | |

|---|---|

| Employees | 1.45 |

| Employers | 1.45 | Self-employed workers | 2.90 |

Unlike OASI and DI, there is no annual maximum on earnings subject to the HI tax. There is an additional 0.9 percent HI tax on earnings over $200,000 for individual tax return filers and over $250,000 for joint tax return filers.

HI also receives income from monthly premiums paid by or on behalf of individuals who are voluntarily enrolled in Medicare Part A.

SMI Financing

Medicare SMI receives financing from Government contributions, premiums paid by enrollees, payments from States, and interest on reserves. For SMI, Government contributions, which are set prospectively based on projected program costs for the year, represent the largest source of income.

Part B and Part D enrollees pay monthly premiums3 that cover most of the costs that the Government contributions do not cover. Under current law, Part B and Part D premium amounts increase as the estimated costs of those programs rise.

In 2023, the Part B standard monthly premium is $164.90. Individual tax return filers whose modified adjusted gross income exceeds $97,000 and joint return filers who exceed $194,000 must pay the standard premium plus an income-related adjustment amount. In 2023, that additional amount ranges from $65.90 to $395.60 per month.

In 2023, the Part D base beneficiary premium is $32.74. However, actual premium amounts charged to Part D beneficiaries depend on the specific plan they have selected. The actual amount for the basic benefit is projected to average around $32 each month for standard coverage in 2023. If Part D enrollees have modified adjusted gross income that exceeds the same threshold amounts listed just above for Part B, they must pay an income-related adjustment amount. That additional amount ranges from $12.20 to $76.40 per month in 2023.

Part D also receives payments from States that reflect the estimated amounts they would have paid for prescription drug costs for individuals eligible for both Medicare and Medicaid if Medicaid was still the primary payer.

Finally, the SMI Trust Fund also receives income from interest on its accumulated reserves invested in U.S. Government securities.

Who Are the Trustees? The Social Security Act established the Social Security and Medicare Boards of Trustees to oversee the financial operations of the Social Security and Medicare trust funds. Further, the Social Security Act requires that the Boards report annually to the Congress on the financial and actuarial status of the trust funds.

By law, there are six Trustees. Four of them serve by virtue of their positions in the Federal Government:

• the Secretary of the Treasury, who is the Managing Trustee,

• the Secretary of Labor,

• the Secretary of Health and Human Services, and

• the Commissioner of Social Security.

The President also appoints two other Trustees as public representatives, and their appointments are subject to confirmation by the Senate. The two Public Trustee positions have been vacant since July 2015.

PROGRAM OPERATIONS IN 2022

How many people got benefits from the programs? At the end of 2022, 57.2 million people received OASI benefits and 8.8 million received DI benefits. Additionally, 65.0 million people were enrolled in Medicare.

How large are the asset reserves in the trust funds right now? At the end of 2022, OASI asset reserves were $2.7 trillion, DI asset reserves were $118.0 billion, HI asset reserves were $196.6 billion, and SMI asset reserves were $212.6 billion. The OASI Trust Fund asset reserves declined in 2022 while DI, HI, and SMI Trust Fund asset reserves increased.

| OASI | DI | HI | SMI | |

|---|---|---|---|---|

| Reserves (end of 2021) | $2,752.6 | $99.4 | $142.7 | $183.0 |

| + Income during 2022 | 1,056.7 | 165.1 | 396.6 | 591.9 |

| - Cost during 2022 | 1,097.5 | 146.5 | 342.7 | 562.4 |

| Net change in Reserves | -40.7 | 18.6 | 53.9 | 29.5 |

| Reserves (end of 2022) | 2,711.9 | 118.0 | 196.6 | 212.6 |

Note: Totals do not necessarily equal the sums of rounded components.

How did program income compare to costs in 2022? In 2022, the OASI Trust Fund’s cost of $1,097.5 billion exceeded income by $40.7 billion. In contrast, the DI Trust Fund’s income of $165.1 billion exceeded cost by $18.6 billion. Combining the experience of the two separate funds, Social Security’s cost exceeded income by $22.1 billion.

The HI Trust Fund’s income of $396.6 billion exceeded cost by $53.9 billion as it continued to receive repayments of accelerated and advance payments ($33.4 billion) made from the trust fund to providers in 2020. At the end of 2022, roughly 99 percent of the accelerated and advance payments have been repaid. The SMI Trust Fund’s income of $591.9 billion exceeded cost by $29.5 billion.

What were the sources of program income in 2022? Program income received from each source is as follows:

| Source | OASI | DI | HI | SMI |

|---|---|---|---|---|

| Payroll taxes | $945.9 | $160.7 | $352.8 | — |

| Taxes on OASDI benefits | 47.1 | 1.6 | 32.8 | — |

| Interest earnings | 63.5 | 2.8 | 4.1 | $3.8 |

| Government contributions | — | — | 1.1 | 422.1 |

| Beneficiary premiums | — | — | 4.8 | 148.9 |

| Payments from States | — | — | — | 13.7 |

| Other | a.2 | b | 1.0 | 3.5 |

| Total | 1,056.7 | 165.1 | 396.6 | 591.9 |

a Includes $0.2 billion in reimbursements from the General Fund of the Treasury

and less than $0.5 million in gifts.

b Less than $50 million.

Additional details and the percentage of total program income received by source are described below:

• Income from payroll taxes—An estimated 180.5 million people paid Social Security payroll taxes in 2022, and 184.4 million people paid Medicare payroll taxes. Income from payroll taxes accounted for approximately 90 percent, 97 percent, and 89 percent of OASI, DI, and HI total income, respectively.

• Income from income tax on Social Security benefits—Income tax on Social Security benefits accounted for 4 percent of OASI income, 1 percent of DI income, and 8 percent of HI income.

• Income from interest on asset reserves—Interest earnings made up 6 percent of total income to the OASI Trust Fund, 2 percent of total income to the DI Trust Fund, 1 percent for the HI Trust Fund, and less than 1 percent for the SMI Trust Fund.

• Federal government contributions—Government contributions accounted for 71 percent of total income and financed 75 percent of SMI Part B and Part D program costs.

• Income from Medicare premiums—Premiums paid by enrolled beneficiaries accounted for approximately 25 percent of SMI total income and 1 percent of HI total income.

• Income from payment from States—State payments covered about 11 percent of Part D costs, accounting for approximately 2 percent of total SMI income.

What program costs were paid during 2022? The 2022 program costs for each of the trust funds are:

| Category | OASI | DI | HI | SMI |

|---|---|---|---|---|

| Benefit payments | $1,088.1 | $143.6 | $337.4 | $556.8 |

| Railroad Retirement financial interchangea | 5.3 | .2 | — | — |

| Administrative expensesb | 4.0 | 2.7 | 5.3 | 5.6 |

| Total | 1,097.5 | 146.5 | 342.7 | 562.4 |

a Funds are shifted between the Railroad Retirement program and the Social Security trust funds on an annual basis so that each trust fund is in the same position it would have been had railroad employment always been covered under Social Security.

b Administrative expenses include expenses incurred by the Social Security Administration, the Department of Health and Human Services, and the Department of the Treasury in administering the programs and the provisions of the Internal Revenue Code relating to the collection of contributions.

Benefit payments accounted for 99 percent of OASI program costs, 98 percent of DI program costs, 98 percent of HI costs, and 99 percent of SMI costs.

Administrative expenses made up 0.4 percent of OASI program costs, 1.9 percent of DI program costs, 1.6 percent of HI program costs, and 1.0 percent of SMI program costs.

PROJECTED TRUST FUND OPERATIONS

Each year, the Trustees project the future cost and income for each of the trust funds for the next 75 years. This section provides the short-range (10-year) and long-range (75-year) financial projections for the OASI, DI, and HI Trust Funds. The SMI Trust Fund is not discussed in this context because Federal law sets premium increases and Government contributions so that annual income matches annual costs.

The Trustees project that the combined OASI and DI Trust Fund reserves will continue to decrease in 2023 because total cost ($1,388 billion) is expected to exceed total income ($1,335 billion). For OASDI, the Trustees project that total cost will exceed total income in all future years, as it has starting in 2021.

The Trustees project an increase in HI Trust Fund asset reserves in 2023, as total income ($407 billion) is expected to exceed total cost ($402 billion). Annual HI deficits are projected to return in 2025 and to persist for the remainder of the projection period.

The key dates for the OASI, DI, and HI Trust Funds are:

| OASI | DI | OASDI | HI | |

|---|---|---|---|---|

| First year cost exceeds income excluding interesta | 2010 | 2044 | 2010 | 2025 |

| First year cost exceeds total income including interesta | 2021 | b | 2021 | 2025 |

| Year asset reserves are depleted | 2033 | c | d2034 | 2031 |

a Dates indicate the first year a condition is projected to occur and then persist each year through 2097.

b Projected annual balances remain positive through 2097.

c The trust fund asset reserves are not projected to become depleted during the 75-year period ending in 2097.

d If the legally separate OASI and DI trust funds were combined, the hypothetical combined OASDI asset reserves would become depleted in this year.

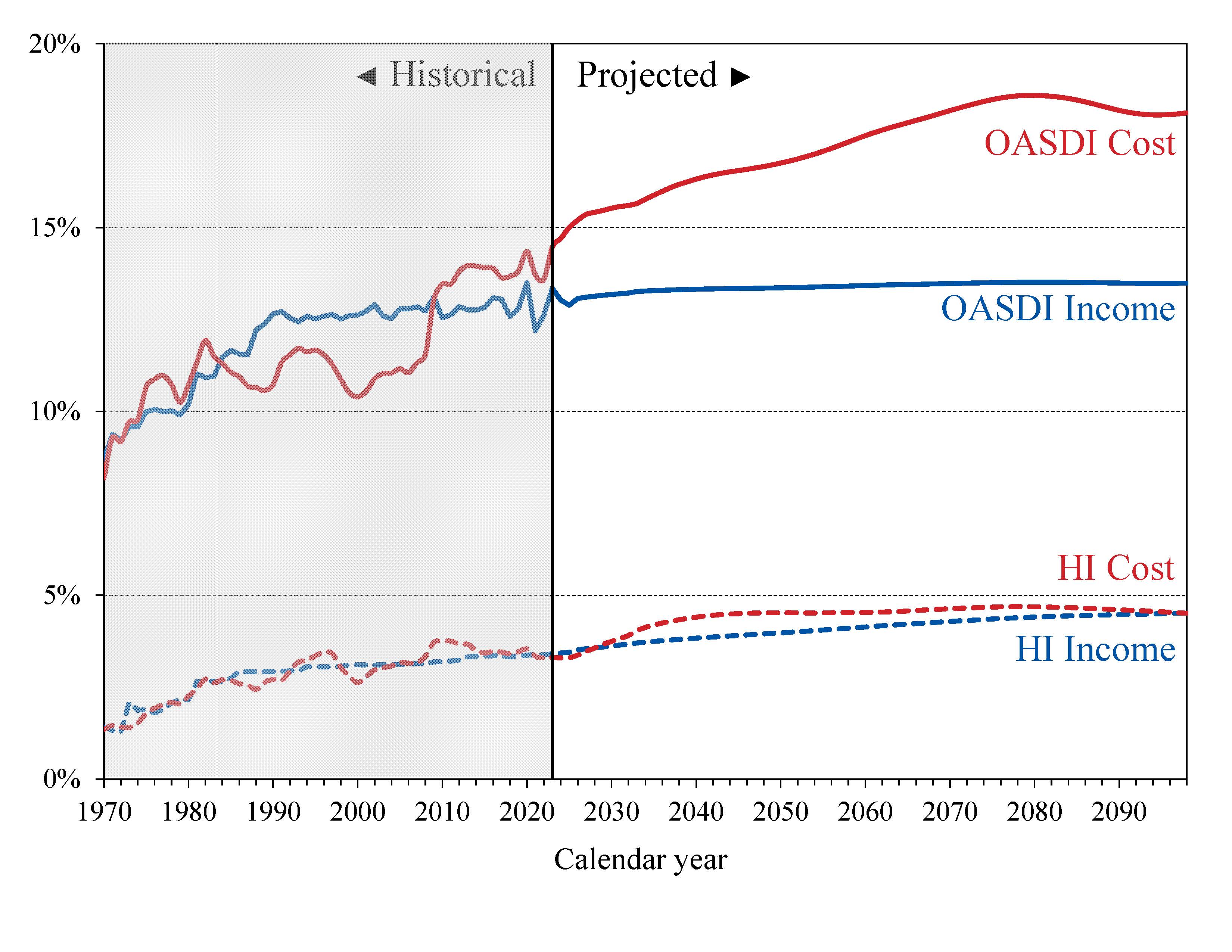

What are the annual income and costs for the trust funds? Because the primary source of income for OASDI and HI is the payroll tax, it is useful when assessing the financial outlook to express the programs’ incomes and costs as percentages of taxable payroll. Chart A illustrates the size of income and cost relative to earnings subject to taxation for each of these programs. In this illustration, interest income is not included in OASDI and HI income. Interest income accounts for a smaller share of program income as trust fund reserves decline.

Chart A—OASDI and HI Income and Cost as Percentages of Their Respective Taxable Payrolls

The percentages shown in Chart A are comparable within each program, but not across programs. This is because the two programs have different taxable payrolls. The OASDI payroll tax is imposed on earnings creditable for Social Security purposes up to an annual taxable maximum amount ($160,200 in 2023) that ordinarily increases each year with the growth in the nationwide average wage. There is no taxable maximum amount applied for the HI payroll tax. In addition, larger numbers of Federal, State, and local government employees are covered under the HI program. Therefore, HI taxable payroll is about 25 percent larger than OASDI payroll.

OASDI

Over time, the projected OASDI annual cost rate rises from 14.53 percent of taxable payroll in 2023 to 18.50 percent of taxable payroll by 2078. It then decreases to 17.75 percent in 2097.

The projected OASDI income rate is stable at about 13 percent throughout the long-range period.

HI

Over time, the projected HI annual cost rate rises from 3.40 percent of taxable payroll in 2023 to 4.83 percent of taxable payroll in 2048. It then slightly declines to 4.66 percent in 2097.

The projected HI income rate rises gradually from 3.43 percent in 2023 to 4.47 percent in 2097. The increase in the HI income rate is primarily due to the higher payroll tax rates for high earners that began in 2013. An increasing fraction of all earnings will be subject to the higher tax rate over time because the thresholds are not indexed. By 2097, an estimated 80 percent of workers would pay the higher rate.

Do the trust funds have an annual surplus or deficit? The difference between the annual income rate and annual cost rate of the trust funds is known as the annual balance. This is calculated for each year in the projection period. When annual costs exceed annual income, a trust fund has an annual deficit. When annual income exceeds annual costs, a trust fund has an annual surplus.

OASDI

The annual deficit in 2022 for the OASDI trust funds was 0.98 percent of taxable payroll. Projected annual deficits for the OASDI program gradually increase from 1.24 percent of taxable payroll in 2023 to 5.06 percent in 2078, and then decline to 4.35 percent of taxable payroll in 2097.

The 2023 reports show larger expected annual deficits throughout the 75-year projection period that are, on average, about 0.13 percentage point higher than those shown in the 2022 reports.

HI

The Trustees project small annual surpluses for the HI Trust Fund, 0.03 and 0.02 percent of taxable payroll, in 2023 and 2024. Beginning in 2025, projected annual deficits expressed as a share of taxable payroll reappear and increase from 0.05 percent in 2025 to a high of 0.92 percent in 2045. During that period, the cost rate will increase primarily due to rising per beneficiary spending and aging baby boomers. Deficits then gradually decline to 0.19 percent of taxable payroll in 2097.

Throughout the long-range period, cost rate growth is constrained by statutorily required reductions to Medicare provider payment rate updates. At the same time, income rates increase as a larger share of earnings becomes subject to the additional 0.9 percent payroll tax and a larger share of Social Security benefits becomes subject to income tax that is credited to the HI Trust Fund.

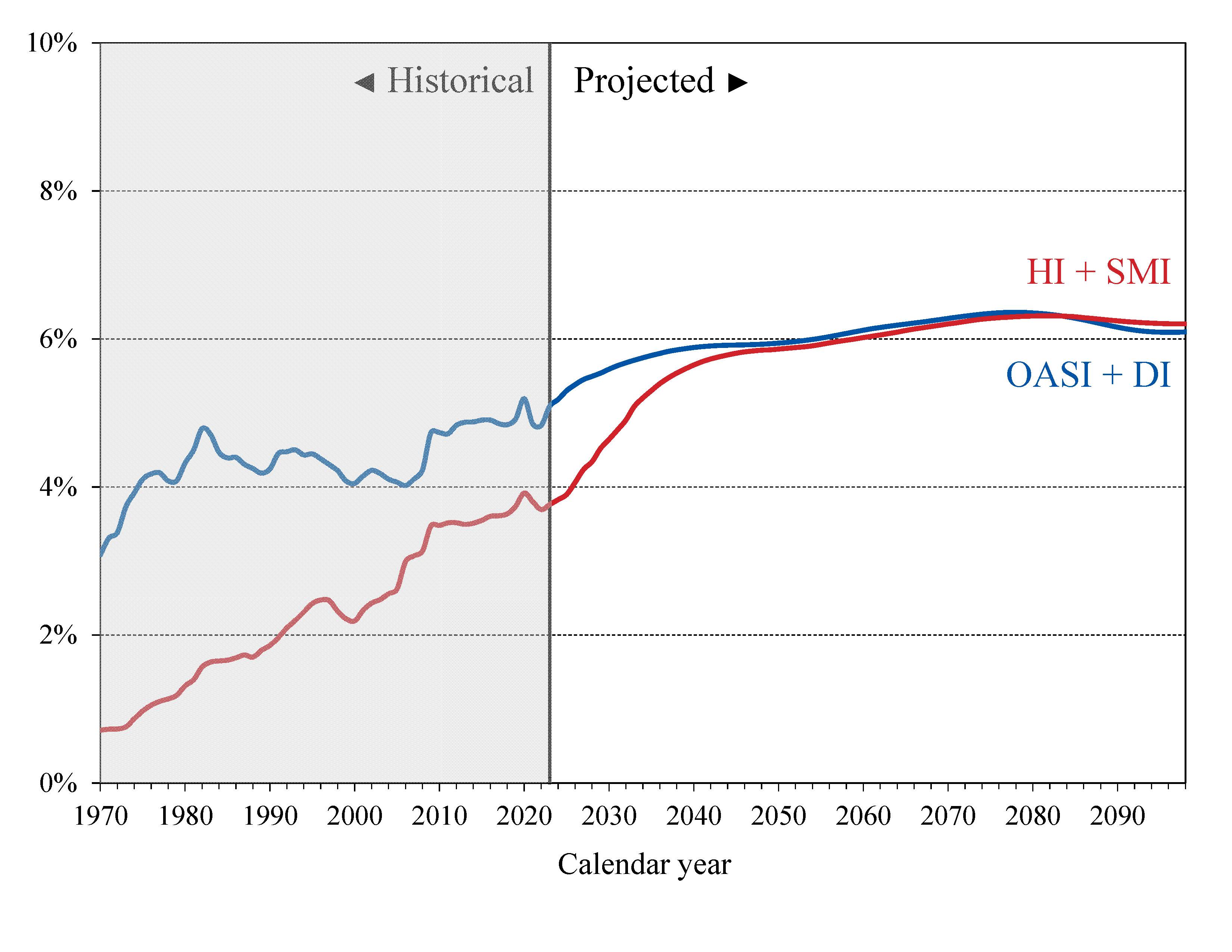

What are the costs and income in relation to GDP? To better understand the size of these projected costs, one can compare them to gross domestic product (GDP), the most frequently used measure of the total output of the U.S. economy. This comparison tells us how much of the nation’s total economic output is needed to finance these programs.

Chart B—Social Security and Medicare Costs as Percentages of GDP

In 2023, Medicare’s annual cost is about 74 percent of Social Security’s annual cost. By 2048, Medicare cost is expected to equal or exceed that of Social Security through 2097.

The costs of both programs will grow faster than GDP through the mid-2030s primarily due to the rapid aging of the U.S. population, and generally continue to increase thereafter at a slower rate through 2076. This is because the number of beneficiaries rises rapidly as baby boomers retire and also because the persistently lower birth rates since the baby boom cause slower growth of employment and GDP.

Social Security (OASI and DI)

The Trustees project that Social Security’s annual cost will increase from 5.2 percent of GDP in 2023 to 6.3 percent in 2076. It then declines to 6.0 percent by 2097. The 75-year actuarial deficit equals 1.3 percent of GDP through 2097, increased from 1.2 percent last year.

Medicare (HI and SMI)

Medicare’s annual cost is projected to rise from 3.9 percent of GDP in 2023 to 6.0 percent by 2045 mainly because of the rapid growth in the number of beneficiaries. Medicare cost then increases to 6.1 percent by 2097 as the health care cost per beneficiary grows, particularly for Medicare Part D.

SMI spending is expected to be 2.3 percent of GDP in 2023, grow to 4.0 percent by 2058, and further increase to 4.2 percent in 2097.

Social Security and Medicare, combined

The combined cost of the Social Security and Medicare programs is about 9.1 percent of GDP in 2023. The Trustees project the combined cost of the programs will grow to 11.5 percent of GDP by 2035 and to 12.1 percent by 2097, with most of the increase coming from Medicare.

The projected costs for the OASI, DI, and HI programs as shown in the charts and described in this summary assume that the full benefits set out in law will continue to be paid. These programs are not allowed to pay any benefits beyond what is available from annual income and trust fund reserves, and they cannot borrow money. Therefore, after the trust fund asset reserves become depleted, the cost of benefits that would be paid is lower than shown in this summary.

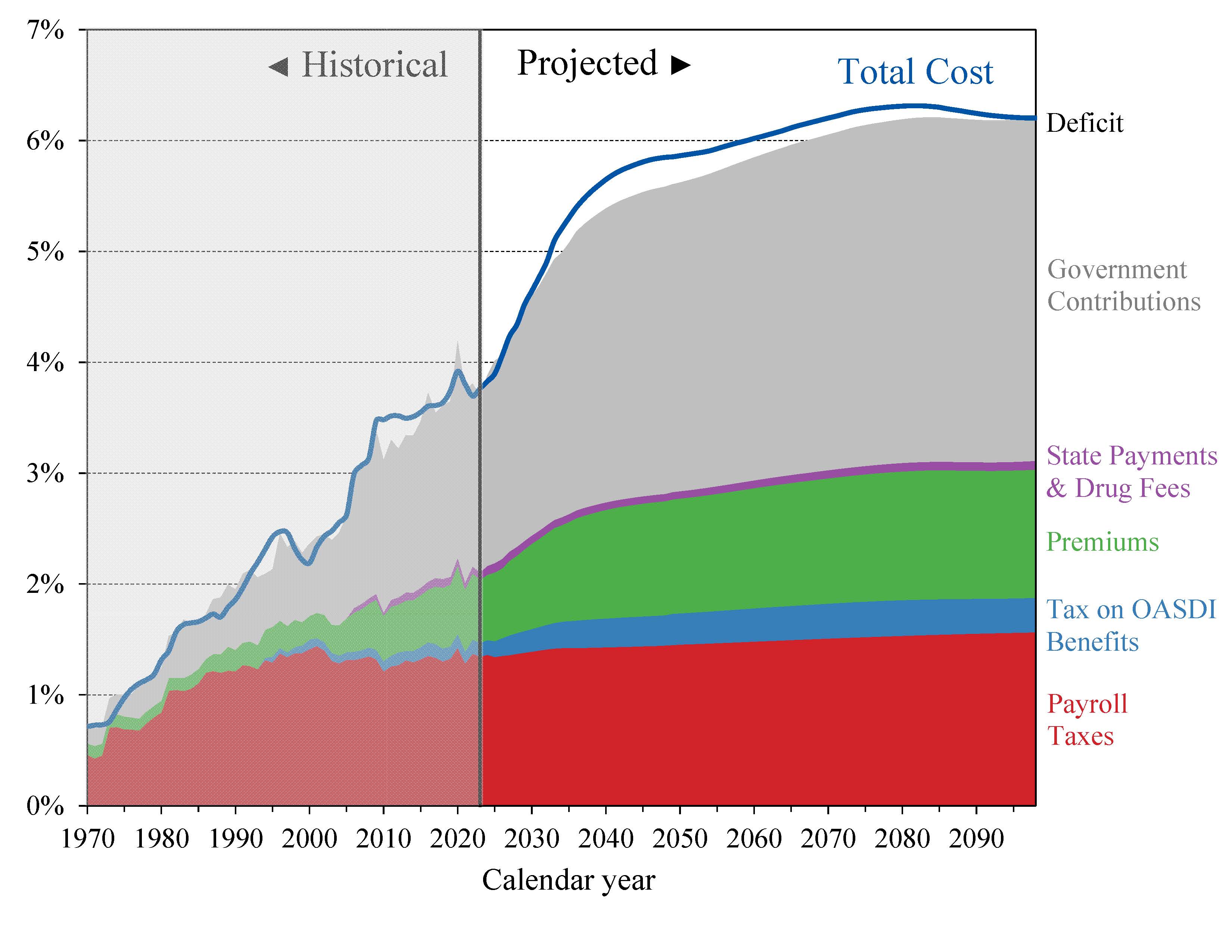

How will cost growth change the sources of Medicare financing? Although Government contributions and beneficiary premiums already account for much of the income for the Medicare trust funds, they finance a growing share of overall Medicare costs.

Chart C shows scheduled cost and non-interest revenue sources under current law for HI and SMI combined as a percentage of GDP. The total cost line is the same as displayed in Chart B and shows that the Trustees project Medicare cost to rise to 6.1 percent of GDP by 2097.

Chart C—Medicare Cost and Non-Interest Income by Source as a Percentage of GDP

Projected revenue from payroll taxes and income taxes on OASDI benefits financing the HI Trust Fund increases from 1.5 percent of GDP in 2023 to 1.9 percent in 2097 under current law.

During the same period, projected Government contributions to the SMI Trust Fund increase more rapidly from 1.6 percent of GDP in 2023 to 3.0 percent in 2097. Beneficiary premiums increase from 0.6 percent of GDP to 1.1 percent. Therefore, the share of total non-interest Medicare income from taxes declines from 39 percent to 31 percent, while the Government contributions share rises from 43 percent to 50 percent and the share of premiums rises from 16 percent to 19 percent.

Medicare’s distribution of financing changes in large part because the Trustees project that costs for Part B and especially Part D increase at a faster rate than for Part A. The projected annual HI financial deficits beyond 2035 are about 0.4 percent of GDP through 2053, and they gradually decline to about 0.1 percent of GDP by 2097. There is no provision under current law to finance that shortfall.

The Implications of High Levels of General Fund Transfer Funding for Medicare

The law requires the Trustees to determine each year whether the proportion of annual Medicare costs funded by certain statutorily defined financing sources, primarily Government contributions to SMI, is expected to exceed 45 percent in any of the next 7 fiscal years. The Trustees determined Medicare funding from Government contributions is expected to exceed 45 percent of total costs in fiscal year 2025.

This is the seventh consecutive report the Trustees made such a determination. Making such a determination triggers a statutory “Medicare funding warning,” which requires that the President submit to Congress proposed legislation to respond to the warning within 15 days after submitting the budget (for FY 2025 due to this year’s warning). The law then requires Congress to consider the legislation on an expedited basis.

PROJECTED TRUST FUND ADEQUACY

The 2023 reports project that the OASI and HI Trust Funds’ asset reserves are insufficient to pay full scheduled benefits throughout the 75-year projection period. The DI Trust Fund is projected to have sufficient income to pay full scheduled benefits throughout the long-range period. The SMI Trust Fund is adequately financed into the indefinite future because current law provides financing from Government contributions and beneficiary premiums each year to meet the next year’s expected costs.

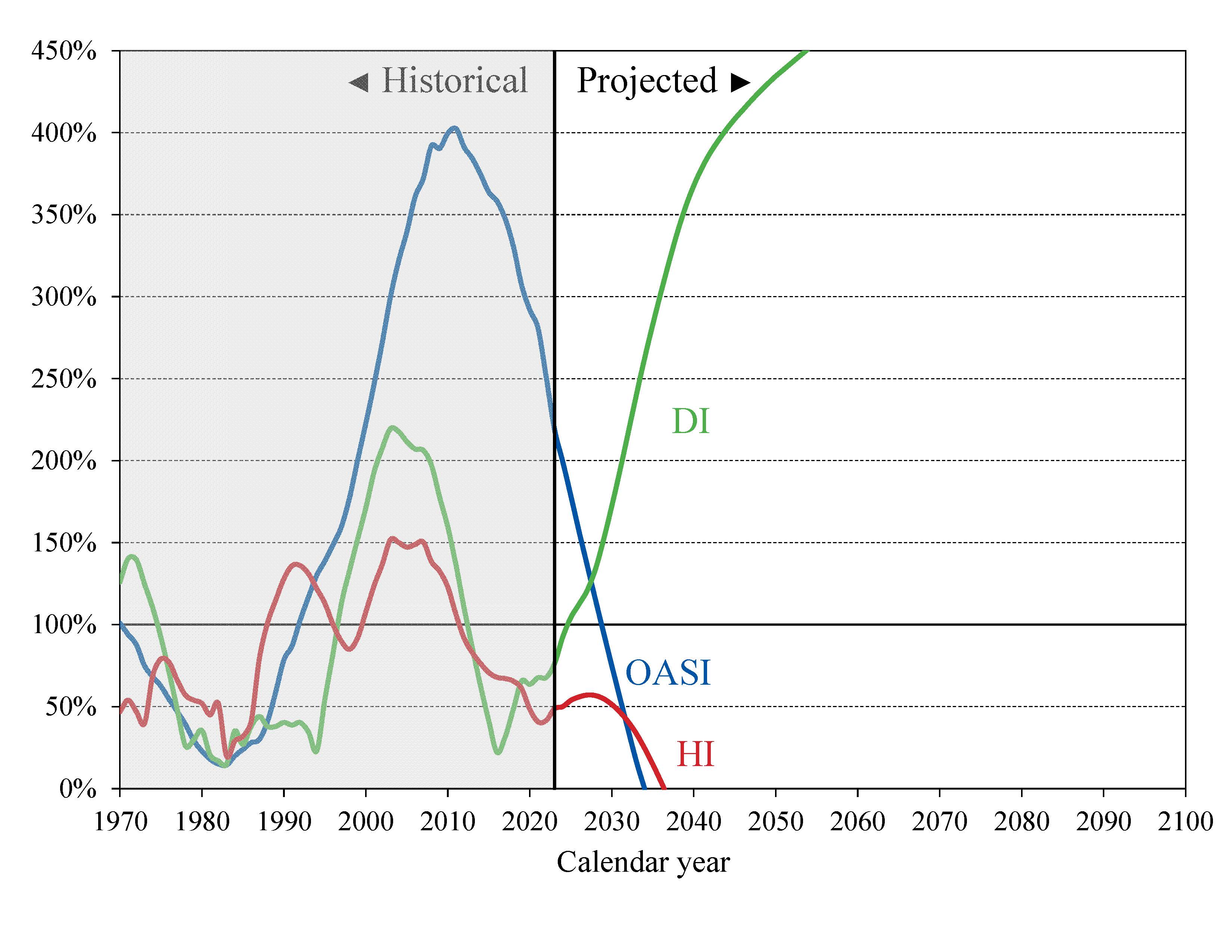

Chart D shows the trust fund ratios for the OASI, DI, and HI Trust Funds throughout the 75-year projection period. The “trust fund ratio” is the value of trust fund asset reserves at the start of a year expressed as a percentage of the projected costs for the ensuing year.

A trust fund ratio of 100 percent or more, or a ratio that is expected to reach 100 percent within 5 years and remain at or above 100 percent through the short-range period, indicates that the fund’s reserves are adequate in the short-range. That level of projected reserves for any year suggests that even if cost exceeds income, the trust fund reserves combined with annual tax revenues would be sufficient to pay full benefits for several years.

Chart D—OASI, DI and HI Trust Fund Ratios

[Asset reserves as a percentage of annual cost]

The financial outlook for the OASI and HI Trust Funds depends on a number of demographic and economic assumptions. Nevertheless, the actuarial deficit in both OASI and HI is large enough that averting trust fund depletion under current-law financing is extremely unlikely.

| OASI | DI | OASDI | HI | |

|---|---|---|---|---|

| Year asset reserves are depleted | 2033 | a | b2034 | 2031 |

| Percent of scheduled benefits able to be paid: | ||||

| At the time of reserve depletion | 77 | a | 80 | 89 |

| For 2097 | 71 | a100 | 74 | c96 |

a The trust fund reserves are not projected to become depleted during the 75-year period ending in 2097. The trust fund ratio is projected to be 159 percent in 2097.

b If the OASI and DI trust funds were combined, hypothetically, the year the combined asset reserves would become depleted.

c The percent of scheduled benefits payable is projected to decline to 81 percent by 2047 before gradually increasing to 96 percent by 2097.

Table 8 summarizes the projected years of asset reserve depletion for the OASI, DI, and HI Trust Funds, as well as the expected percent of scheduled benefits that could be paid from program income at the time of asset reserve depletion and at the end of the 75-year projection period.

What is the outlook for short-range trust fund adequacy? For the 75-year projection period, the short-range accounts for the first 10 years, which is 2023 through 2032 for the 2023 reports. The short-range adequacy of the OASI, DI, and HI Trust Funds is measured using the trust fund ratio.

The Trustees apply a less stringent annual “contingency reserve” test to SMI asset reserves. The financing for each part of SMI is considered adequate if it is sufficient to fund all services provided, including benefits and administrative expenses, through a given period (generally, through the end of the current calendar year).

To account for the possibility that cost increases under either part of SMI will be higher than expected, the trust fund accounts need assets that are adequate to cover a reasonable degree of variation between actual and projected costs. For the SMI Trust Fund, the Trustees consider the adequacy for Part B and Part D separately.

The outlook of the trust funds over the short-range period is as follows:

• The OASI Trust Fund is not adequately financed throughout the short-range period. Its trust fund ratio is projected to decline from 220 percent at the beginning of 2023 to 91 percent at the beginning of 2029.

• The DI Trust Fund is projected to be adequately financed throughout the short-range period. Its trust fund ratio is projected to increase from 77 percent at the beginning of 2023 to 107 percent by the beginning of 2026, the fourth projected year, and continues increasing for the remainder of the short-range period.

• The HI Trust Fund is not adequately financed throughout the short-range period and has not been since 2003. Its trust fund ratio is 49 percent at the beginning of 2023 and is not projected to attain 100 percent within 5 years.

• For SMI Part B, the Trustees estimate that the financing established through December 2023 will be sufficient to cover benefits and administrative costs incurred through the current calendar year and that assets will be adequate to cover potential variations in costs as a result of new legislation or cost growth factors that exceed expectations.

• For SMI Part D, the Trustees estimate the financing established for Part D, together with the flexible appropriation authority, would be sufficient to cover benefits and administrative costs incurred through 2023. The Centers for Medicare & Medicaid Services calculate Part D premiums paid by enrollees based on the plan bids such that Part D revenues annually cover estimated costs. This flexible appropriation authority established by lawmakers for Part D allows additional financing through Government contributions if costs are higher than anticipated.

What is the outlook for long-range trust fund adequacy? The long-range period is a 75-year valuation period, which is 2023-97 for the 2023 reports.

The long-range adequacy of the OASI, DI, and HI Trust Funds is measured using the actuarial balance.4 The actuarial balance captures how expected income for the 75-year projection period compares to the expected costs for the same period, as a percentage of taxable payroll.

A negative actuarial balance (a deficit) indicates that estimated income is insufficient to meet estimated trust fund obligations for all or part of the 75-year period. A positive actuarial balance (a surplus) indicates that estimated income is more than sufficient to meet all obligations.

A projected negative actuarial balance represents the average amount of change in income or cost that is needed over the 75-year period in order to achieve an actuarial balance of zero. An actuarial balance of zero indicates that costs can be met for the 75-year period with existing asset reserves and expected income, leaving asset reserves at the end of the period equal to the following year’s cost.

The long-range actuarial balances for the OASI, DI, and HI Trust Funds are:

| OASI | DI | OASDI | HI | |

|---|---|---|---|---|

| Actuarial balance | -3.62 | 0.01 | -3.61 | -0.62 |

• The OASI Trust Fund has a projected long-range actuarial deficit equal to 3.62 percent of taxable payroll, compared to 3.41 percent in the 2022 report.

• The DI Trust Fund now has a projected long-range actuarial surplus equal to 0.01 percent of taxable payroll, compared to a 0.01 percent deficit in the 2022 report. The DI Trust Fund is in actuarial balance for the 75-year period.

• The combined OASDI trust funds now have a projected long-range actuarial deficit equal to 3.61 percent of taxable payroll, compared to 3.42 percent in the 2022 report. The increased actuarial deficit is due to recent economic experience and changes in near-term economic assumptions. The Trustees have lowered the levels of GDP and labor productivity in response to new data on inflation and output.

• Medicare’s HI Trust Fund now has a long-range actuarial deficit equal to 0.62 percent of taxable payroll, compared to 0.70 in the 2022 report. This change is mainly due to: i) lower health care utilization through 2032 due to updated expectations for health care spending following the onset of the COVID-19 pandemic, and ii) higher taxable payroll in most years resulting from the changed economic and demographic assumptions.

A one-time, uniform increase in the payroll tax rate for all years starting in 2023 would be sufficient to achieve an actuarial balance of zero for the OASI and HI trust funds. Nonetheless, the relatively large variation in annual deficits implies that this approach would result in large annual surpluses early in the 75-year projection period but increasing annual deficits in later years. Sustainable solvency beyond the end of the 75-year period would require larger payroll tax rate increases and/or benefit reductions than those needed on average for this report’s long-range period (2023-97).

CHANGES REFLECTED IN THE 2023 REPORTS

How does this outlook for Social Security compare to last year's? This year’s report indicates that the expected year of depletion of asset reserves in the OASI Trust Fund has moved forward by one year to 2033. The DI Trust Fund is again projected to be able to pay full benefits through the end of the 75-year projection period.

| 2023 Report | 2022 Report | Change | |

|---|---|---|---|

| OASI | 2033 | 2034 | 1 year earlier |

| DI | a | a | N/A |

a The trust fund reserves are not projected to become depleted during the 75-year period.

If these two legally separate trust funds were combined, then OASDI trust fund asset reserves hypothetically would be projected to be depleted in 2034, 1 year earlier than projected in the 2022 report.

The actuarial balance for the OASDI trust funds worsened in the 2023 report, with a 0.19 percentage point decrease.

| OASI | DI | OASDI | |

|---|---|---|---|

| Shown in the 2022 report: | |||

| Actuarial balance | -3.41 | -0.01 | -3.42 |

| Changes in actuarial balance due to changes in: | |||

| Legislation / Regulation | a | a | a |

| Valuation period | -.05 | -.01 | -.05 |

| Demographic data and assumptions | -.03 | a | -.03 |

| Economic data and assumptions | -.04 | a | -.04 |

| Disability data and assumptions | a | .01 | .01 |

| Methods and programmatic data | -.08 | .02 | -.06 |

| Total change in actuarial balance | -.21 | .02 | -.19 |

| Shown in the 2023 report: | |||

| Actuarial balance | -3.62 | .01 | -3.61 |

a Between -0.005 and 0.005 of taxable payroll.

Note: Totals do not necessarily equal the sums of rounded components. A negative actuarial balance is a deficit.

The changes in the actuarial balance were due to the combined effects of changes in methods and program data, advancing the valuation period by one year, and revisions in economic and demographic data and assumptions. The following changes had the largest effects on the actuarial deficit:

• There were improvements in projection methods and new data. The method for specifying the age distribution of new lawful immigrants has changed, more recent data are used to project the average benefits of newly entitled worker beneficiaries, and there was an update to post-entitlement benefit adjustment factors (which account for differences in mortality by benefit level and post-entitlement earnings).

• The 75-year valuation period advanced from 2022-96 to 2023-97, which adds a high-deficit year (2097) into the calculation.

• There have been revisions in economic data and assumptions. Since the projections in last year’s report were set, the Trustees have reassessed their expectations for the economy in light of recent developments, including updated data on inflation and output. Consequently, they have lowered the projected levels of GDP and total economy labor productivity by about 3 percent over the projection period.

• There were changes in demographic data and assumptions. These include slightly lower projected birth rates in the earlier years of the long-range projection period, higher near-term death rates related to the COVID-19 pandemic, and the incorporation of new population data on immigration, marriage, and divorce.

How does this outlook for Medicare compare to last year's? The expected year of depletion of the asset reserves in the HI Trust Fund has improved since the 2022 reports.

| 2023 Report | 2022 Report | Change | |

|---|---|---|---|

| HI | 2031 | 2028 | 3 years later |

HI income in the short range is projected to be higher than last year’s estimates because both the number of covered workers and average wages are projected to be higher. HI expenditures through the short range are projected to be lower than in last year’s report mainly as a result of updated expectations for health care spending following the COVID-19 pandemic. Due to multiple factors, fee-for-service per capita spending has been consistently below pre-pandemic projections throughout the public health emergency, even into 2022 as the pandemic had diminishing effects on much of the economy and the health care delivery system. Several of these factors are now assumed to have a greater impact on the path of spending over the next few years.

The actuarial status for the HI Trust Fund improved in the 2023 report, with a 0.08 percentage point increase in the actuarial balance.

| HI | |

|---|---|

| Shown in the 2022 report: | |

| Actuarial balance | -.70 |

| Changes in actuarial balance due to changes in: | |

| Valuation period | -.01 |

| Base estimate | .16 |

| Private health plan assumptions | .05 |

| Hospital utilization assumptions | -.07 |

| Other provider assumptions | .03 |

| Other economic and demographic assumptions | -.08 |

| Total change in actuarial balance | .08 |

| Shown in the 2023 report: | |

| Actuarial balance | -0.62 |

Note: Totals do not necessarily equal the sums of rounded components. A negative actuarial balance is a deficit.

Several factors contributed to the decreased actuarial deficit. The following changes had the largest effects on the decline:

• Lower health care utilization through 2032 due to updated expectations for health care spending following the onset of the COVID-19 pandemic.

• Higher taxable payroll in most years resulting from the changing economic and demographic assumptions.

The projected Part B costs as a share of GDP are lower than the estimates in the 2022 report due to the expected impact of drug price negotiations of the Inflation Reduction Act (IRA) and updated expectations for medical care use after the peak of the COVID-19 pandemic. They continue to increase at a faster rate than GDP.

The Part D projections as a percentage of GDP are significantly lower than in last year’s report primarily as a result of the impact of drug price negotiations and other price growth constraints included in the provisions of the IRA.

CONCLUSION

The 2023 Trustees Reports indicate a need for substantial changes to address Social Security’s and Medicare’s financial challenges. The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust their expectations and behavior. Implementing changes sooner rather than later would allow more generations to share in the needed revenue increases or reductions in scheduled benefits. With informed discussion, creative thinking, and timely legislative action, Social Security and Medicare can continue to protect future generations.

2 The actuarial balance for the 75-year valuation period is the difference between the summarized income rate and the summarized cost rate as percentages of taxable payroll. When that balance is negative, or is an “actuarial deficit,” projected income over the valuation period plus any trust fund reserves at the start of the period are insufficient to pay all program costs over the period and leave an adequate “contingency reserve” at the end of the period. For the 2023 reports, the valuation period is the 75-year period between 2023 and 2097.

3 The premium for certain low-income beneficiaries is paid on their behalf by Medicaid for Part B and by Medicare for Part D.

4 The actuarial balance is not relevant for the SMI Trust Fund, because Federal law sets premium increases and Government contributions at the levels necessary to bring the SMI Trust Fund into annual balance.

A MESSAGE FROM THE PUBLIC TRUSTEES

Because the two Public Trustee positions are currently vacant, there is no Message from the Public Trustees for inclusion in the Summary of the 2023 Annual Reports.