Number: 104-3

Date: March 21, 1995

HOUSE WAYS AND MEANS CHAIRMAN BILL ARCHER

THE OMNIBUS CONSOLIDATED RESCISSIONS

SSI AND ALIENS, RET AND TAXATION OF BENEFITS

On March 13, 1995, Ways and Means Committee Chairman Bill Archer introduced the Personal Responsibility Act (H.R . 1214) and the Contract with America Tax Relief Act of 1995 (H.R. 1215). These two bills supersede the earlier Contract with America bills which contained SSA-related provisions--the Personal Responsibility Act (H.R. 4, H.R. 1157) and the Senior Citizens' Equity Act (H.R. 8), respectively.

THE PERSONAL RESPONSIBILITY ACT (H.R. 1214)

The full Ways and Means Committee reported the Personal Responsibility Act (H.R. 4) as a clean bill (H.R. 1157) on March 8, 1995 (see Legislative Bulletins 104-1 and 104-2 dated March 7, 1995 and March 13, 1995, respectively.) As introduced, H.R. 1214 includes the provisions of H.R. 1157 with the following modifications.

Restricting Welfare for Noncitizens

Rather than making all aliens ineligible for 35 spec ified Federal welfare programs as under H.R. 1157, H.R. 1214:

- Prohibits any Federal means-tested public benefits to aliens not lawfully present in the United States and to al iens lawfully present as nonimmigrants with exceptions for noncash, in-kind assistance (including emergency medical care) and certain housing programs.

- Provides that immigrants, with certain exceptions , would not be eligible for five Federal programs- -SSI , temporary assistance for needy families under title IV of the Social Secur ity Act, social services block grant assistance, Medicaid, and food stamps-but would not be prohibited from other Federal means-tested public assistance programs.

Also provides that spouses and dependent children of veterans, Armed Forces

personnel on active duty, their spouses , and dependent child ren are added to the

categories of immigrants that are exempted.

Expansion of the Federal Parent Locator Service

- Requires HHS to transmit to SSA, for ver ification purposes, certain inform ation about individuals and employers maintained under the Federal Parent Locator Service. SSA would be requi red to ver ify the accuracy of, correct, or supply to the extent possible, and report to HHS the name, SSN, and birth date of individuals and the employer identification number of employers. SSA would be reimbursed by HHS for the cost of this verification service.

Collection and Use of SSNs for Use in Child Support Enforcement

- State child support enforcement procedures would have to require that the SSN of any applicant for a professional license, commercial driver's license, occupational license, or marriage license be recorded on the application . Also, the SSN of any person subject to a divorce decree, support order, or paternity determination or acknowledgement would have to be placed in the pertinent records.

House floor debate on H.R . 1214 is expected to begin today .

THE TAX RELIEF ACT OF 1995 (H.R. 1215)

The full Ways and Means Committee reported the Contract with America Tax Relief Act of 1995 on March 14 without amendment. The legislation contains the same SSA-related provisions included in the ear lier Contract with America bill (H.R. 8).

Repeal of Increase in Tax on Social Secur ity Benefits

- Repeals the 1993 taxation provision that increased the taxable portion of Social

Security and Railroad Retirement Tier I benefits from 50 to 85 percent for single

beneficiarie s whose adjusted gross income is over $34 ,000 and married beneficiaries

filing jointly whose adjusted gross income is over $44,000.

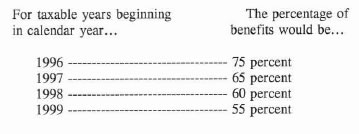

The provision would phase-in the repeal of the higher rate for taxpayers with incomes in excess of the above thresholds as follows:

For taxable years beginning after December 31 , 1999, Social Security and Railroad Retirement Tier [ benefits would be treated as under the law pr ior to 1994 (no more than 50 percent of benefits taxable).

Adjustment in Exempt Amount of Retirement Earnings Test

- Gradually raises the earnings limit for those age 65 to 69 to $30,000 by the year 2000.

The increase would be phased-in over 5 years as follows:

The provision would be effective for taxable years beginning after 1995.